Are you feeling disenchanted with the high fees your bank is charging? Or perhaps you’re looking for a new way to make your money work harder for you while still giving you easy access to your funds.

The answer to your banking questions is closer than you think.

Credit unions, like PSECU, offer numerous advantages to their banking institution counterparts and can help you achieve financial freedom. The benefits credit unions offer – such as competitive rates on loans, solid returns on investments, free or low-cost checking and savings accounts, financial education services, and free or low-cost ATM access – might help you understand why there are more than 5,800 federally insured credit unions operating in the United States.

There were 106.2 million credit union members in the United States as of September 2016 – an indicator of their popularity.

We’re proud to be part of the credit union movement. In fact, we were one of first to be chartered in Pennsylvania. Because we believe strongly in what credit unions can do for consumers, we offer this primer to show how credit unions are smart alternatives to banks, including the similarities between and differences of banks and credit unions, the benefits of credit unions, and the reasons you should switch to a credit union.

What is a Credit Union?

Credit unions and banks are similar in one important way: both offer their members or customers valuable financial products. These products span a wide range and may include checking and savings accounts, certificates of deposit, loan products, credit cards, and access to funds via ATMs or electronically.

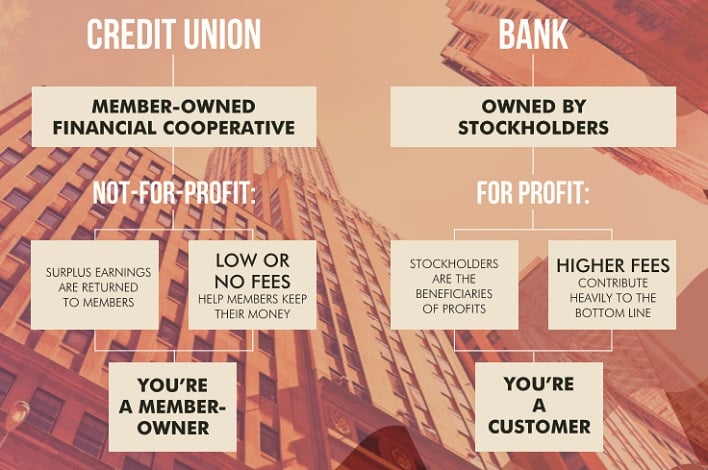

One key difference is who owns the institution and benefits from you banking there. Credit unions are member-owned and exist to serve members, not drive profits for a bank owner or stockholders.

Like banks, credit unions do take precautions to make sure your money is safe.

Federally insured credit unions – accounting for about 98% of all U.S. credit unions – offer you a safe place to deposit funds, just like a bank does. The National Credit Union Administration Insurance Fund insures credit unions and provides the same protections that the FDIC provides banks: insurance coverage of up to $250,000* per share owner, per insured credit union, for each account ownership category.

Profits, Purpose and Structure of Banks vs. Credit Unions

When you look at the structure of a bank, you’ll see that they are for-profit businesses that are held by either private owners or stockholders. Therefore, banks concentrate on earning profits, which are distributed back only to their owners, not their customers. Since owners and stockholders generally want to make the largest profit possible, that profit often may come by offering lower-quality customer service, higher interest rates on loans, and fee-based checking accounts.

In comparison, credit unions are not-for-profit and member-owned. Each member, or account holder, has an ownership stake in the entity: one member, one vote. Credit unions generally have two overarching goals:

- Provide members affordable, easy-to-obtain services

- Redistribute profits back to members

Credit unions are represented by a volunteer board of directors, which any member is allowed to run for and become elected to. You become a member of a credit union through your initial deposit. This deposit establishes your ownership stake, makes you a part owner and gives you an equal voice in the credit union’s decisions, directions and future.

Credit unions work diligently to serve their members, not themselves. A credit union’s surplus earnings are returned back to members, sometimes in the form of higher interest rates on savings accounts, discounted rates on loans or additional banking services. Some credit unions also provide benefits such as financial education, retirement planning classes or college scholarships.

As financial cooperatives, credit unions operate under seven principles established by the International Cooperative Alliance that highlight the commitment to serving members and communities:

- Voluntary membership. Membership is open to anyone within the credit union’s field of membership, and discrimination isn’t allowed.

- Democratic member control. Each member has a voice as to the decisions that are made.

- Members’ economic participation. When members invest more money in a credit union, the credit union has the resources to provide additional services at a low cost.

- Autonomy and independence. As autonomous entities, it’s the members who control the organization.

- Education, training and information. Credit unions understand the importance of providing training to members, the Board of Directors, employees, and the general community, especially in the area of financial literacy.

- Cooperation among cooperatives. Working together is the key to a credit union’s success. The CO-OP Network, which gives credit union members wide and free access to ATMs, is an example of credit union collaboration.

- Concern for community. Credit unions focus on members, but they also help the larger community, understanding that a thriving community will help the credit union become more successful.

Credit Union Eligibility

While anyone can join a bank, you must be eligible to join a credit union and take advantage of their products and services. Because credit unions serve specific groups and are owned by the members who use their services, there are rules pertaining to who can join.

There are many different kinds of credit unions, giving nearly everyone an opportunity to become a member. Each credit union is established by its particular membership field. For example, there are several large credit unions that address the financial needs of those who have served or are serving in the military. Another example is the “local” credit union that serves residents of a defined region. Click on the photo below to learn how you can join PSECU.

Credit Union Account Accessibility

With more resources and finances at their disposal, many banks can offer bells and whistles, such as investments in emerging technology or breadth of products. They also have numerous branches nationwide, and accessibility to ATMs gives customers many opportunities to take care of business.

In the past, accessibility was a serious limitation of credit unions – but no longer. Technology has opened the door for easy banking without ever having to leave your home.

In addition, some credit unions have opted to share ATMs, offering members more convenient access to both cash and services nationwide. The CO-OP network offers nearly 30,000 ATMs, which means many credit union members have direct and surcharge-free access to their money.

What Benefits Do Credit Unions Offer?

Frequently misunderstood as exclusive – and perhaps elusive – organizations, it should be now clear that credit unions are very accessible. Modern credit unions provide an impressive array of services and offer many benefits. If you’re wondering whether credit unions are better than banks for your financial situation, this list of benefits may help you decide.

Personalized Service

Do you want to feel like more than a number? Since credit unions often serve a specific group or region, credit unions can seamlessly offer more personalized attention.

It’s hard to put a price on developing a working relationship with a trusted financial professional – and customizable service is something that big-name banks can’t always offer.

Increased Customer Satisfaction

The CFI Group reports that in 2015, the customer satisfaction level of credit union members was among the highest of all industries measured, more than 8 points above the score for banking customer satisfaction.

Since we began our feedback program in 2014, we’ve received more than 50,000 responses. Overall, our members consistently express their appreciation for the quality of service they receive from us, and the value their PSECU membership brings to their lives.

Member-Owned

One of the main benefits of credit union membership is that credit unions are member-owned. The goal of a credit union is to provide financial services at a reasonable cost – not charge members with fees.

As a result, they have the flexibility to decide how much they want to charge for their products and services. And management is dedicated to taking revenues and reinvesting them into services for members or minimizing members’ costs. That can add up to big savings for members.

Better Rates Across Product Lines

Need a little more bang for your buck? Credit unions may provide just what you’re looking for. Because credit unions are not-for-profit organizations, they pass their financial benefits on to their members. In contrast, banks need to turn a profit for owners, so they’re less likely to provide financial incentives to customers.

You’ll first notice this advantage in the form of significantly higher interest rates on deposit accounts, such as money market, checking and savings accounts – even certificates. Credit unions also offer the same financial products as banks – including mortgages, personal loans, car loans and credit cards. But at credit unions, you’ll find comparatively lower annual percentage rates.

When you’re paying interest on an auto loan over 60 months, getting the lowest possible interest rate makes a significant impact on monthly payments and the overall interest the borrower pays. This makes credit unions an appealing choice for loans and lines of credit.

So if you’re in the market for a loan – or simply want your money to work harder for you – check out a local credit union to see if they can offer better rates and lower fees than a bank can provide.

Lower Fees

If you’re looking to save on fees, you should definitely consider a credit union. With a plethora of accounts requiring no minimum balance or monthly service charge, you can recognize significant savings over the course of a year when you choose a credit union.

If you find a bank offering free checking, is it really free? Or are there numerous “fine print” qualifications? Are you restricted on the number of ATM withdrawals you can make per month? Can you write only a certain number of checks monthly before you’re obligated to pay a fee? Are you required to have direct deposit set up?

Credit unions offer several account options, often with fewer restrictions, obligations, and complications. You might recognize savings with other fees, such as overdraft and bounced check fees. While you’ll still be obligated to pay a fee for these services as a credit union member, you’ll likely pay less than you would as a bank customer.

Unexpected Perks

The benefits credit unions offer aren’t just financial. Other nontraditional perks that credit unions may offer include:

- College scholarships for high school students

- Product discounts for members

- Coupons for entertainment options

- Free financial education programs for kids and adults

- Online services, such as planning calculators, budgeting tools, and spending tips

- Donations to the communities they serve

Should I Switch to a Credit Union?

Credit unions are great options for many people, and they provide a range of perks that big banks simply cannot, such as a better, more personalized banking experience.

If you’re looking for lower rates on loans and higher rates on savings accounts, you’ll usually find them at your local credit union.

Being part of a larger credit union that’s working to help its members achieve their financial goals isn’t insignificant. Working together to make spending and saving easy, cost-effective and rewarding is what credit unions are all about.

It’s easy to find a home at a local credit union, and joining one can be simple. But it’s important to find one that offers the services you need and the convenience you desire. As a safe, reliable alternative to banks, credit unions can help you take the next step toward establishing a solid financial future.

What Are the Benefits of Joining PSECU?

PSECU – founded more than 80 years ago by 22 state employees – has grown into one of the largest credit unions in Pennsylvania. Membership extends beyond state employees to include students, faculty and staff at many Pennsylvania universities and colleges, as well as hundreds of businesses that have entered into the PSECU field of membership as a company benefit. Our more than 400,000 members and almost $5 billion in assets gives us the ability to provide superior financial products, online tools, financial education workshops and top-notch service.

We also offer scholarships to members graduating from high school, a wide variety of lending products and more. With our Founder’s Card, you can earn 1.5% cash rewards on purchases. See the PSECU Visa® Founder’s Card Rewards Program Terms and Conditions for full details. Our lending and refinancing solutions have helped members save more than $20 million in just two years, and since 2013, we’ve returned more than $52.5 million in Relationship Rewards to members.

We’re committed to giving back to our community and helping you achieve your financial goals. It’s what makes us different. We work as your trusted financial partner to make smart decisions that help your money work harder and smarter for you.

As a Pennsylvania resident, there are many ways for you to join PSECU and start taking advantage of the services we offer. If you’re ready to take the next step, we’re here to help. It’s never too late – or too early – to invest in your future. Luckily, PSECU makes it easy for you to do just that.

Find more money management tips and resources on our WalletWorks page.

*All PSECU deposit shares, including checking, Regular, additional savings, money market and certificates, are federally insured by the National Credit Union Administration (NCUA) up to $250,000, the maximum allowed by law. In addition to the $250,000 of insurance provided on an individual account or combination of individual accounts, you are also insured up to $250,000 for any combination of accounts you may hold jointly with other individuals.