You’ve created your budget, and you know what you’ll have to do to afford your expenses while putting some money aside for savings. But, if you have some time before you do move out, it’s a good idea to save a little extra.

In this chapter, we’ll share practical tips to help save for getting your first apartment and living alone for the first time. This will provide information that supplements your budget-building process to make your move as successful as possible.

How Much Money Should I Save Before Moving Out?

In chapter 2, we shared the importance of setting aside a three- to six-month emergency fund to cover necessary expenses if unexpected situations arise. But, that doesn’t mean saving should stop there.

There’s no set rule for what amount should be saved in addition to your emergency fund, or how much you’ll need to be financially prepared to move out, but the following guidelines and statistics may provide a starting point for you to set your goals.

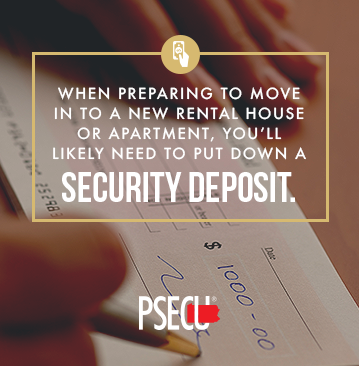

Start by considering the cost of rent and your security deposit. When preparing to move in to a new rental house or apartment, you’ll likely need to put down a security deposit. This money is collected by landlords, and it’s used to repair damages that might occur during the length of time you occupy the property. In most cases, this amount is equal to one month’s rent. When you vacate the property, the deposit will be used to make repairs, with the balance returned to you after they’ve been completed.

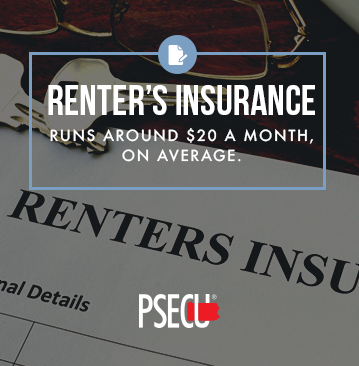

Another consideration relates to renter’s insurance. In some rental situations, renter’s insurance is required to rent a home or apartment. It’s your responsibility to purchase and maintain your renter’s insurance policy and keep it current. A 2014 study found that 56% of renters between the ages of 23 and 35 did not have renter’s insurance, which runs around $20 a month, on average, even though 68% of those surveyed believed it would cost over $5,000 to replace their personal belongings damaged in the event of a fire or other unfortunate situation. Renter’s insurance should not be neglected — it’s one of the most important ways you can protect yourself and your belongings.

Moving costs may be an additional expense as you prepare to move out on your own. Many costs can be saved by handling the move on your own with help from friends and family. However, if you do rent a truck or enlist the help of moving professionals, be prepared to spend several hundred dollars. If you’re paying out of pocket for a move, check with a tax professional about what receipts you should keep to take advantage of possible savings later.

We discussed utilities as being an important line item for your budget. While the actual cost of utilities varies — and the number can be affected greatly by your behavior — you should be prepared to spend around $100-$500 on monthly utilities. Remember, some of these may be covered by the landlord, so it’s important to ask what’s included so you’re aware of how much to budget for.

Actual living expenses will vary from one individual to another. Begin tracking what you spend each month now, and consider the costs you may not currently contribute toward. These will become yours when you live on your own.

Lastly, consider your monthly student loan bills, credit card payments and other debt you may have accrued. The average student debt is around $37,000 for a 2016 graduate, which makes for a significant monthly payment.

How to Save Money

You know what you need to make your move as successful and affordable as possible. Now, it’s time to make it happen. There are steps you can take today to start saving money effectively. Some may be much easier to act on than you would anticipate.

Start by creating a dedicated savings account. It’s easy to think about the bank account you currently deposit money into and write checks or pay bills from as the only account you’ll ever need. However, putting money in a place that’s separate from your spending account might be in your best interest. When money is harder to access, it can be easier to save for more important purchases and life events down the road.

The old cliché may be true: Out of sight, out of mind. Keep your savings separate from your spending account for best results.

Another great way to save is to set up a form of automatic savings. There are many ways to save money before you have a chance to see it or think about it, which may be easier than physically moving the money yourself. Talk to your Human Resources department at work about options for setting aside a certain amount of money each paycheck. If this is not an option or you’d like to do more, consider other options for saving automatically:

- Set up your checking account to automatically transfer a certain amount of money each month into a separate account.

- Use the PSECU Savings app to “sweep” your remaining change, daily or one-time, to your savings share or “scratch” to reveal an amount of money that goes straight toward your savings goal.

- Keep track of purchases you normally make, but skip — think coffee, manicures, eating out — and put the money you would have spent into a dedicated savings account. The Savings app can help with this, too.

Saving doesn’t have to mean setting aside large amounts of money at a time. Instead, it can be painless, automatic and even fun.

While setting up automatic savings options, practice the 24-hour rule when you’re about to buy. When you decide you want to make a purchase, wait 24 hours to do so whenever you can. This 24-hour period provides extra time to consider that purchase against long-term savings goals and could help curb spending tendencies that work against what you’re trying to accomplish.

Sometimes, one of the biggest problems with saving is first understanding where your money is actually going. You think you’re doing well. You aren’t making large purchases, but somehow, saving isn’t happening.

To overcome this challenge, use PSECU’s budgeting worksheet, referenced in chapter 2, regularly and honestly. Recording each purchase brings it to your attention and holds you accountable, which may make more of an impact than swiping a credit card. By understanding how the small purchases add up, you can be more mindful of where you’re spending and where there’s room to save.

In some cases, unexpected amounts of money may be given to you. These can come in the form of gifts, tax returns or bonuses at work. When they present themselves, it’s easy to splurge — to go on a trip or make a big purchase you’ve been dreaming of. What if you saved the money instead? What could that do for your long-term goals? Think it through before spending.

Start Saving Now

We want to provide you with the insight and guidance you need to save as effectively as possible. The more you understand various savings options like money market accounts, savings accounts, checking accounts and more, the better prepared you’ll be to start a new, independent life on your own.

It’s easy to think about big goals in life as things to think about tomorrow, or sometime in the future. If you’re not planning on moving out right away or if you’ve decided to give yourself time before making any big decisions, one thing you can do to reach that goal sooner — rather than later — is to start saving today. Waiting will only delay your opportunity to move out on your own.

Saving for living on your own doesn’t have to be an insurmountable challenge. It’s something you can absolutely accomplish with a few small steps, starting right now. Have questions? We’re here to help.

Read Our Other Chapters

- Chapter 1: Questions to Consider Before Moving Out

- Chapter 2: How to Budget for Living on Your Own

- Chapter 3: How to Save to Live Alone for the First Time

- Chapter 4: How to Find Your New Space

- Chapter 5: How to Move Out and Get Started

- Chapter 6: How to Manage Groceries, Cleaning, and More

- Chapter 7: What College Students Need to Know Before Living on Their Own

- Chapter 8: Tips for Living Alone